Maximizing Roth IRA Savings

A Roth IRA is an individual retirement account funded with after-tax money. For those who qualify, a Roth IRA can be an integral part of not only an individual’s retirement savings, but also can be used to fund financial goals throughout his or her lifetime.

Why Roth Now

Hedging Future Tax RatesIf tax rates increase or you fall in a higher tax bracket in the future, Roth IRA funds can still be distributed tax-free.

Need for Retirement Savings

Due to the uncertainty of Social Security and longer life expectancies, saving more for retirement in a variety of investment vehicles should be a priority.

Compounding Tax-Free Growth

Earnings including dividends, interest, and capital gains that accrue in a Roth IRA are tax-free year over year.

Benefits for Investors

Flexibility and Access to AssetsRoth IRA contributions may be withdrawn tax- and penalty-free at any age and for any reason. Earnings can also be withdrawn at any age; however, they will generally be subject to taxation and a 10% penalty unless at least five years have passed from the first Roth IRA funding and the account owner has reached age 59½.

The 10% early withdrawal penalty on earnings is waived for distributions used to pay for qualified education expenses, health insurance, unreimbursed medical expenses, first-time home purchase up to $10,000, and for individuals on active military duty.

Tax-Free Money and Tax Diversification

Tax-free money in retirement provides significant advantages. By not increasing income when taking retirement account withdrawals, Medicare premiums and Social Security taxation may be unaffected. Also, by having Roth IRA money at an individual’s disposal, he or she can plan which retirement accounts to withdraw from to remain in a favorable tax bracket.

No Required Minimum Distributions

Traditional IRAs and 401(k)s generally require distributions starting at age 72. Roth IRAs do not have this requirement.

Estate Planning

Upon the account owner’s passing, Roth IRAs will be transferred to beneficiaries. Heirs will then have access to tax-free money and can continue to stretch the earnings in the Roth IRA over their life expectancy or for 10 years following the account owner’s passing.

Tips for Roth IRA Savings

Contribute Early in the YearRoth IRA contributions for 2022 can be deposited from January 1, 2022 – April 15, 2023. By making contributions early in the year, the assets have more time to potentially grow.

Make Annual Contributions a Priority

By missing even a single year of contributions, the IRA owner may miss out on significant tax-free earnings.

Variety of Ways to Fund

Roth IRAs can be funded via contribution, conversion, and/or rollover. For high earners, the backdoor Roth is available.

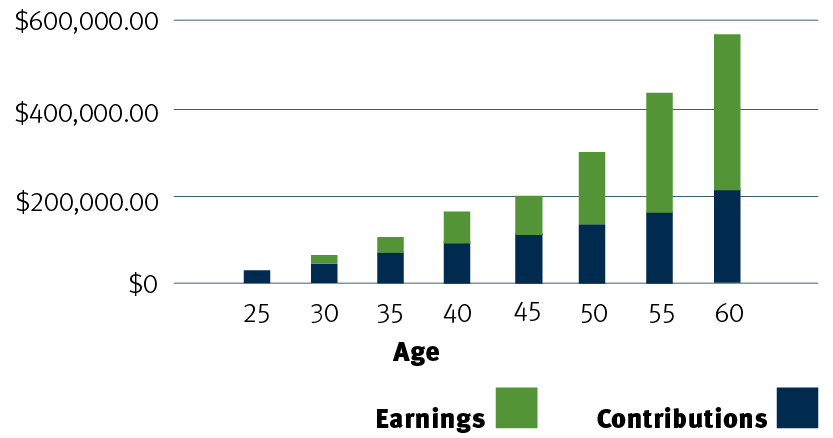

Tax-Free Growth Example

At age 25, John contributes $6,000 to a Roth and continues to contribute each year for the next 35 years. At age 50, he increases his annual contributions to $7,000. Based on a 5% annual return, John would have $582,225 that he can distribute tax-free at age 60.

This is a hypothetical illustration only and does not represent actual results of any investment.

If you’re not funding a Roth IRA, you may be missing out on an exceptional opportunity. Contact a Stifel Financial Advisor today to find out how a Roth IRA may benefit you.

Stifel does not provide tax advice. It is always recommended that you seek the aid of a competent tax advisor or accountant to assist with tax advice and guidance.

1221.3946473.1